Grandmother’s wisdom and Gold Investment – What does the data say? What should the Investors do.

Gold has run up a lot recently with people exclaiming about the wisdom of their grandmothers and Indian Women in general who own 11 % of the Gold that was ever mined, about 24000 tons. To give you a context this is more Gold than that held as reserve by the top 5 Gold owning countries (Government treasury) put together.

I’m sure our grandmother’s had a lot of wisdom, but with times we have changed our life to suit our needs and objectives. In the same way, let us review the most common perceptions of Gold and see if the data supports it.

Is gold truly a safer asset with better returns? Let’s examine the data.

Discover how the traditions of Dhanteras align with the principles of long-term investing. Explore key lessons on wealth-building, patience, consistency, and diversification inspired by this festive celebration.

Dhanteras, celebrated as the first day of Diwali, marks the beginning of a festive period that is steeped in tradition, prosperity, and wealth accumulation. On this auspicious day, people buy gold, silver, and other valuables with the belief that these investments will bring good fortune and long-term wealth. Interestingly, the essence of Dhanteras aligns closely with the principles of long-term investing, both of which emphasize discipline, patience, and future rewards.

In this article, let’s explore how the philosophy behind Dhanteras holds lessons for effective long-term investing and how these two concepts intersect in building lasting wealth.

1. Dhanteras Teaches Us to Invest Early and Smart

On Dhanteras, families make it a tradition to invest in assets like gold, silver, and even property. These purchases are not meant for instant gratification but are assets expected to grow in value over time, protecting wealth against inflation.

Similarly, starting investments early—whether in mutual funds, stocks, or real estate—allows time to work in your favor through compounding returns. Just as gold appreciates in value over the years, disciplined financial investments grow exponentially when held for the long term.

Lesson: The earlier you start investing, the more wealth you accumulate through compounding.

2. Patience is Key: Both in Tradition and Markets

Purchasing gold on Dhanteras is not about using it immediately but rather about holding it patiently as a store of wealth. The same principle applies to long-term investing. Investors who are patient and remain invested through market cycles reap the rewards, even during downturns.

Markets, like any investment, go through ups and downs, much like the fluctuations in the price of gold. The ability to ride out volatility is critical to achieving long-term financial success. Those who sell off assets prematurely miss out on the eventual recovery and growth.

Lesson: Just like gold is held for years to reap benefits, investments should be held patiently to experience growth.

3. Diversification: Gold and Beyond

On Dhanteras, people don’t limit themselves to just gold but often buy silver, utensils, and other valuables. This tradition reflects a form of diversification—investing in different assets to spread risk.

In long-term investing, diversification is just as essential. A well-balanced portfolio with a mix of stocks, bonds, and other assets ensures that your investments are protected from market volatility. A diversified strategy ensures that losses in one area don’t wipe out your overall wealth.

Lesson: As we spread wealth across different valuables on Dhanteras, spread your investments across various financial assets to manage risk effectively.

4. Consistency Matters: Yearly Rituals and SIPs

Dhanteras is not a one-time event but an annual tradition, reinforcing the habit of saving and investing consistently. Similarly, systematic investment plans (SIPs) in mutual funds or automated contributions to retirement funds promote regular, disciplined investing, ensuring that wealth grows steadily over time.

Whether it’s buying gold every year or investing monthly through SIPs, small but regular contributions accumulate into significant wealth over the years. This consistency ensures that you don’t need to time the market to build wealth effectively.

Lesson: Like the yearly practice of Dhanteras, consistent investing ensures steady financial growth over time.

5. Both Build Legacy and Security

The gold bought on Dhanteras is often passed down as a family heirloom, becoming a symbol of legacy and security. Similarly, long-term investments provide financial stability for future generations, whether through inheritance or savings for education, retirement, or emergencies.

Investing isn’t just about growing wealth for yourself—it’s about creating a financial foundation for your loved ones. Just like Dhanteras emphasizes security for the family, long-term investing secures financial peace for the future.

Passing on the Family Heirloom

Lesson: Both Dhanteras and long-term investing build lasting wealth that can be passed down to future generations.

Conclusion: Wealth That Grows, Year After Year

Dhanteras and long-term investing share a common goal: creating wealth that grows steadily and lasts for generations. Both traditions underscore the importance of patience, consistency, and diversification. Whether you’re buying gold or investing in the stock market, the underlying principle is the same—wealth is built over time, not overnight.

As you celebrate Dhanteras this year, think of it as more than just a shopping festival. It’s a reminder to start or strengthen your long-term financial plans. Gold may glitter, but compounding returns in your investments shine even brighter. This Diwali, light the lamp of prosperity not just with gold but with a commitment to long-term investing.

11 Strangest Secrets of Wealth Creation revealed by Top Asset Management Company CEO’s

CEO’s of Indian AMC’s which manage over 50,000 Crores of Investor Money came together in this event conducted by Network FP to share the strange yet simple secrets of Wealth Creation for the benefit of over 10,000 investors.

Secret 11 – Godfather of Wealth : Trust India’s growth Story

India’s growth story and transformation was shared by Mr. Navneet Munhot of HDFC MF. This especially in contrast with the turbulent times in Europe (Russia – Ukraine War), China’s Banking Crisis etc. The burgeoning SIP book has also reduced structural risk of FII’s and has provided the market a lot of stability.

The Story of Two Cities : Shangai Index and Mumbai (Sensex)

While China’s GDP and corporate profits has grown rapidly in the last 10 years from 2003 to 2023, Shanghai Index has merely doubled from 1500 to 3000. However during the same period Indian markets have become 25x. World is beginning to see India as a premium market and the next 25 years is expected to look even better.

Wealth Creation = Sound Investment + Time + Patience

Secret 10- Multiplier of Wealth : Participation in Equity Markets

This secret of Wealth Creation was presented by Mr. A Balasubramanian of ABSL MF.

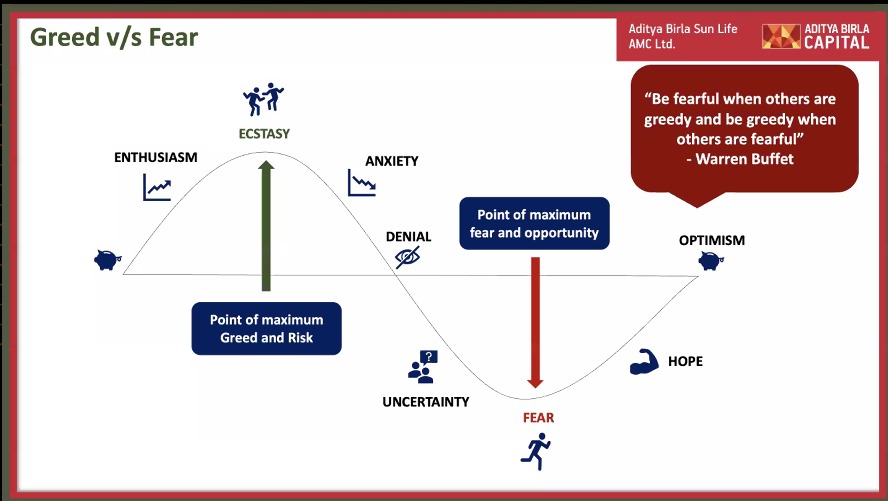

The Optimistic, entrepreneurial , new generation prefers to raise Equity capital over Debt unlike the previous generation. Markets Volatility causes ebb of Greed and Fear in Investors and it is necessary to work with a professional to avoid being subjected to it and exiting at the wrong time.

Why Equity?

-> Markets are Volatile By Nature. Stay Invested through the cycles. -> Equity Outperforms All Asset classes. -> Have Optimism, Stay Invested by taking guidance from professional

Secret 9- Super Power of Wealth: Youngistaan

This Secret of Wealth Creation was ably presented by new mother and Edelweiss CEO Ms.Radhika Gupta.

From the hapless and hopeless Generation Y (1960 -1980) the Optimistic Millenials (1981- 1996) and the Exuberant Gen Z have come a long way in their outlook.

50% of India is young i.e 550 mn people who spend over $500 Bn . They are also 55% of New investors and have contributed to over 1.5 Cr in SIP in the last 5 years. Over 80 % of them prefer to invest in Equity.

Start an SIP Piggy Bank when they are young. Talk to them about it and encourage them to save and allow them to spend their saving once goal is reached.

Wealth and Youth: Points to remember

-> Shape habits Early and give them a head start -> Pass on Values by sharing your money stories. Else they will learn from Social Media -> Be honest about money with your children -> Take the right risks at right time -> Pass on Legacy in a liquid portfolio and not illiquid portfolio like land, buildings

Talking to Kids about Math and money be like …

Secret 8 – Simplifier of Wealth : Be Disciplined with SIP’s

This secret of Wealth Creation was presented by Mr. G. Pradeep Kumar, CEO, Union Mutual Fund.

SIP has become more popular than Mutual Funds. But due to our fascination to gamble, we have more investors in crypto than Folio’s in Mutual Funds. All of us are emotional about our investments and SIP is the best way to take the emotion out of our investing.

-> Best way to participate in India is through Equity -> Best Way to participate in Equity is through Mf’s -> Best way to Invest in MF’s is through SIP’s

-> Start Small Start Now -> Increase SIP by 10 % every year as income goes up and reach your goals faster -> Stay Invested and withdraw only for goals -> Personal finance Professionals help you stick to the discipline

Secret 7 – Commander of Wealth: Mind Your Investment Behaviour

Swarup Mohanty, CEO, Mirae MF presented about the quirks of Investor behaviour that causes them to get lower returns from their investments and proves an obstacle in wealth creation.

Process of A Financial Plan:

Step 1: Meet your Advisor Step 2: Discuss Your Goals Step 3: Get your Risk profile Assessment done Step 4: Make a Financial Plan Step 5: Make appropriate Scheme Selection Step 6: Do Periodic Review

Most people want to skip straight to Step 5.

The real star of a Financial Plan is the Goal. The Rockstar of the plan is the one who help you get there.

Mr. Swaroop Mohanty, CEO, Mirae

-> Right Investment is not about return generation, but risk mitigation. Are you staying closer to your risk profile ? -> Best time to buy is when you have money -> Make Volatility is your friend. It helps us to buy assets at good prices. -> Beware of Behavior Bias – Loss Aversion, Herd Mentality, Market Bias, Asset class risk

Secret 6- All Rounder of Wealth : Strength of Asset Allocation

The strength of Asset Allocation through Multi allocation funds was presented by Mr.Kalpen Parekh, DSP MF.

-> There is no consistent winning asset class. Right combination can get better returns than any individual asset class with less volatility. -> Multi – Asset/Hybrid gives ability to say ‘I don’t know and I don’t Care’ about all external noises and geo political changes -> 11 Dhoni’s Vs 1 Dhoni + Good Bowlers + Good Batsmen – which makes a better team? -> US and India pricing currently reflect the optimism. Will the future winners be from elsewhere?

Secret 5 – Defender of Wealth: Tax Efficient Investments

Tax is the biggest single item of expense for Most of us and the need for tax efficient instruments was discussed by DP Singh, SBI MF.

-> Need to consider tax laws to ensure tax efficiency of investments -> Conservative Hybrid and Arbitrage Funds may be considered for Debt Allocation as per current tax laws -> Use Systematic Transfer Plan as a way to protect wealth -> All cars even a Ferrari with an experienced driver needs brakes.

Secret 4 – Goal Keeper of Wealth: Goal Based Investments

The need for Goals to drive Investment decisions was driven home by Mr. Vishal Kapoor, CEO, Bandhan MF.

-> KYG – Know your Goals -> One may different risk profiles for different goals -> Chase Goals not returns.

Investing without Goals is like wandering in a desert with no markers.

Vishal Kapoor , Bandhan MF

One should have a goal, direction and milestones to know if one is progressing in the right path or not.

Goal based investments enable Investors to be objective oriented and disciplined. It also prevents them from reactive actions such as chasing past performance, unnecessary churn and suboptimal returns.

Investing success is all about having a plan and sticking to it with discipline.

Secret 3- Protector of Wealth : Minimize Risk and Maximize Returns

Mr.Rajiv Shastri, CEO, NJ Mutual Fund spoke about Wealth Protection

-> Returns can be generated only through conviction – > Develop conviction through Patience, Discipline, Longevity, Diversification, Asset allocation, Risk Management, Expectations Management -> Volatality is the PRICE of admission for the PRIZE of Superior Returns -> Equity Volataility is not the unknown but known. But in long term of 15 yrs have NO chance of losing money.

Secret 2 – Motivator of Wealth: Aim and Achieve Financial Freedom

The buzz word of the youth on Financial Freedom was covered by Ajit Menon, PGIM Fund backed by the exhaustive market research that PGIM had conducted in this regard.

-> Parents should not be your Emergency Fund and Children should not be your retirement Plan. ->Mongevity – Money + Longevity. Money must last through early retirement and lengthening lifespans -> There is only one financial goal for which you receive no loan – Retirement -> Convert your passion into an income. 36 % have and 39 % considering secondary income either through skills or investments -> Renew , Recharge , Never Retire

Secret 1 – Well Wisher of Wealth: Work with a Professional

-> Total Investing Life could be over 70 + years with 10 – 12 market drops of 20 % and a few 40 % drops. Work with a professionals to tide through the hard times. -> 3 Essential Professionals – A doctor to protect your Health, A Lawyer to protect your assets and A Personal Finance Professional to protect your Lifestyle. -> Share proper data and information with the Finance Professional. -> Take 50:50 responsibility initially when you start working with a professional. -> Do regular reviews.

Secrets of Wealth Creation: Event Summary and Learnings

Simple And Effective Ways to build Generational Wealth Creation is to Work with a Qualified Professionals who will be your guide who enables you to achieve goals through right planning, risk management and implementation.

What does Lakshmi and Kubera teach us about wealth and its various forms?

MahaLakshmi and Navratri Pooja

We recently completed Navratri or the 9 auspicious days in sharadya month where devi or Goddess mother is celebrated in Nine forms on the different days. The 10th day or dasami is celebrated as the Vijayadasmi in the south and Dussera in the north. It is considered as day of the victory of good over evil.

The three main forms of the devi are Goddess Shakti, Goddess Lakshmi and Goddess Saraswati. Since we are a financial blog, let us focus on Goddess Lakshmi and what we can learn about wealth building from this festival and our mythology.

Kubera, the demi- God

Kubera

Hindu Mythology also has a demi-God Kubera, who is associated with wealth. Laughing Buddha is also a form of Kubera. Kubera is the lord or the keeper of wealth. In puranas, he is described as short (dwarf) , overweight, with missing teeth, missing eye and other physical deformities. Stories show him as jealous and showoff.

Lakshmi, the Goddess of Wealth

Goddess Lakshmi

Goddess Lakshmi, the goddess of wealth on the other hand is the epitome of beauty. In India, when an elderly person compliments the a bride to be, they always say ‘She looks like Mahalakshmi.’ It means the girl will bring all good things to the family with her. And it is indeed the highest compliment one can give from their perspective.

Why is there such a stark difference between Kubera and Lakshmi ? Why is Kubera, all things ugly while Lakshmi is the epitome of beauty and perfection. Was it intentional and if so why?

Hindu epics are always very deep and nuanced with lessons to be learnt in every single story, character and description

I contemplated on this and have penned down my thoughts here. You may have a different outlook and if so feel free to share in comments.

Kubera’s story and secret of his wealth:

Kubera is the treasurer or keeper of wealth. This wealth was bestowed to him by Lord Siva. Some stories says it was assigned to him by his Father. He is surrounded by things that are expensive like gold, precious stones, gems etc. He carries with himself a drawstring bag of Gold coins.

Skill Vs Luck

Kubera derives his sense of importance from the wealth that was bestowed on him due to the grace of God. It was not earned through skill or work and may be considered primarily through Luck. If Kubera falls out of the good grace of God and loses his wealth, he loses his identity. There is no way for his to earn back that wealth. As against someone who believes in his own ability to be able to create value and hence wealth. This is how entrepreneurs in various fields, successful specialists such as designers, artists, sportsmen, surgeons etc make their wealth. This is also why first generation entrepreneurs that have built their business and wealth feel more confident even when their luck turns bad and they lose most of their wealth. They believe they created wealth once and they can do it again.

Elon Musk – The Story of Resilience

Elon Musk and the companies he started/owns now

We have many comeback stories of entrepreneurs. My favourite is that of Elon Musk. Elon Musk made most of his early wealth from being co founder of X.com which later became paypal and was bought by E-Bay in 2002 for $1.5 Billion.

Most would have retired into a beach shack and never worked a day in their life. But not Elon Musk. He invested almost all of the money from the Exit into two new companies – SpaceX in 2002 and Tesla in 2004. There were times he barely had money to pay salaries and was at the brink of failure.

But he made a comeback. Space X had a successful launch after several early failures. Tesla is one of the most coveted names in the Auto Industry now. He has created more companies in the field of Energy (Tesla Energy), OpenAI (Promoting and Developing AI), Neuralink (To link Artificial Intelligence with Human Brain) and the Boring Company(To construct Tunnels). Today, Elon is the richest man in the planet. He has created huge wealth and value having come from nowhere (a first generation immigrant) and being close to broke. This is all because of his belief in able to solve problems that people would care about. And this is what people who suddenly get lots of wealth don’t have.

Hoarding:

Uncle Scrooge and his treasury

In a way Kubera is like the Uncle Scrooge in Duck Tales whose happiness comes from rolling over in the gold and hoarding more and more of it. Hoarding is a result of greed and insecurity which comes from Kubera’s inability to replicate his fortune if and when he loses it.

This is also why eventually he loses the throne of Lanka to his half brother Ravana who did not even have an army at his disposal. Ravana won the throne and all the wealth of Lanka without a fight.

Show – off /Arrogance:

This is the other extreme of hoarding where one spends money just to get attention/importance. This is how most people who won lottery or inherit huge wealth lose their fortune. Kubera too out of his arrogance and with an intention to show off his wealth rather than out of devotion or love arranged a feast for Lord Shiva and Goddess Parvati. Shiva knew Kubera’s intentions and instead sent his son Ganesha for the pompous feast.

Ganesha not only ate the huge feast with aplomb, he also started eating the valuable treasures of Kubera from his treasury to satisfy his hunger. Kubera realised his mistake and took refuge in Lord Shiva who quenched Ganesha’s hunger with a ladoo.

My learning from these stories is that ‘Wealth does not give one the feeling of Abundance on its own’. So how is Goddess Lakshmi the epitome of all things good?

Wealth is not just of Money:

Ashta Lakshmi

Goddess Lakshmi manifests herself in 8 different forms or Ashta Lakshmi. The eight forms are Aadhi Lakshmi( the origin or the one who liberates) Dhana laksmi(goddess of wealth), Dhayriya lakshmi/veera lakshmi(goddess of courage), Dhanya lakshmi( Goddess of grains/food), Gaja Lakshmi (Goddess of Animal wealth aka elephants), Santana Lakshmi (Goddess of Offsprings i.e children), Vidya Lakshmi (Goddess of Learning) and Vijaya Lakshmi (Goddess of Victory).

Lakshmi is bestower of Courage, Food Grains, Children, Salvation, Knowledge, Animals (Elephant), Wealth(Prosperity) and Victory. So Mahalakshmi’s grace completes your life in every aspect and is not unidimensional of only financial prosperity as in the case of Kubera.

The aspects of Knowledge/Wisdom and Courage are those that can help one create wealth and value and not be dependent on other’s good grace to become prosperous. That is why self-made people rebuild their lives even when impacted with huge calamities. This is exactly opposite of Kubera who lost his kingdom to his half brother Ravana.

Humble:

Despite being the Goddess of Wealth and the epitome of perfection, she humbly submits herself to the Lotus feet of Lord Vishnu. Such a contrast to Kubera who tries to show off to the the God who was the one who granted the wealth to him. It is through humble servitude it is possible to keep wealth for several generation together. This is the secret of various business families of Parsis’, Jains, Agarwals and other business families who have built and preserved wealth over multiple generations. These families teach their children to be humble and work with values and attitude of being the servant leader.

Wealth Vs Cashflow – The most important difference

One key difference is that Kubera’s wealth is shown as a treasure of Gold and precious stones. These assets are a good store of value but do not multiply or generate cashflow(income) on its own. However Goddess Lakshmi’s wealth is shown as a shower of gold coins from Her hands. Goddess Lakshmi can generate more where it came from but Kubera can not. In this basic difference lies the difference in every behaviour trait we have discussed till now.

Many who have had crores of property have lost the properties due to their inability to pay property tax. The high value property in such cases has been a liability and not an asset. Robert Kiyosaki talks about these concepts in his book Rich Dad Poor Dad.

Wealth Vs Cashflow – My Experience

So is there any real difference between wealth and cashflow. There is and I have personally experienced the same too.

In 2017, My husband Harikrishna Natrajan and I took a break from our work and went on a one year trip around the country. I had dreamt about this trip for a very long time and it was a common goal for us both. We saved up for the trip, we arrived at a budget that was doable for us considering our then networth, spending habits on similar short trips and the time it may take for us to come back and restart our careers.

The Good and the Bad

With the exception of a few days, we lived well within the daily budget we had assigned for ourselves and completed the trip at a cost less that what we had budgeted and saved for.

It was a trip of a life time where we learnt so much about our country and enjoyed it immensely. There are some regrets though. For Eg, When we were in Aleppey, the boat house costed about Rs. 8000 per night. This was significantly more than our daily budget. But from a net worth perspective it may not have left a dent. But we chose to pass on the opportunity telling ourselves that we will come back later. It’s been 5 + years we have not been there yet. We wanted to take my parents but my Father is not around anymore for us to take him there. The covid and the lockdown made us realise we cannot take the future for granted.

There were a few other experiences too that we passed off like this due to a similar thought process.

Realisation : Wealth Vs Cashflow

I look back and realise what drove my/our thought process on these decisions. Although we had a good net worth, a back up plan, considerable confidence in our abilities to come back and start up, we had very little cashflow at that time and were spending almost entirely on our savings. My fear of running out of money kept me too conservative. Some people go all the way to the other extreme and end up spending a life time of money in just a few years and go bankrupt too.

A place we stayed over during a recent weekend trip

Right now, We do not feel that way. For we have built a good cashflow from our investments that more than covers our basic expenses. So we feel abundant and indulge more on experiences, learning, giving etc, the way we had never done before. We know that our pot will never be empty because it is constantly getting refilled.

The thought process is very different and I can truly feel abundance which I never felt when we had wealth but no cashflows or as a salaried person.

Conclusion:

The abundance outlook is one of the reasons one has to attempt to create regular cashflow over appreciating assets that take money out of your pocket. This is especially important while trying to plan for goals such as retirement where you will need a certain sum for living expenses over a long period of time. This is different than accumulating a huge lumpsum which is required for purposes of event planning such as children’s higher education or wedding that requires a large sum during a short period of time.

Do consider these points when you plan for your retirement. If you need any assistance on the same, do reach out to me. May Goddess Lakshmi bless you all with skills, courage and knowledge to obtain all forms of wealth in abundance.

Personal Finance Planning is often confused with frugal living, investment planning etc. What is it ? and What is it not?

What is Personal Finance Planning Not:

Not living Small

Personal Financial Planning is

Not about cutting back on your lattes or Kappis Not about Taking the public transportation Not about having a frugal wedding Not about being cheap Not about giving up your avocado sandwich or chappan bhog Not about buying a hatchback instead of a Sedan

Not Getting Massive Returns on your investments

Not about getting double digit returns with low or no risk. Not finding the next Multi Bagger Stock. Not about investing in exclusive opportunities known to no one else Not about buying at the bottom of the market and selling at the top Not about finding the one mutual fund which will fulfill all your needs Not about investing in a hundred different instruments in the name of diversification Not about becoming a millionaire/ billionaire.

What is Personal Finance Planning about then?

It is about

Knowing yourself. Knowing what is truly important to you and prioritizing it. Not compromising the long term goals for the short term impulsive wants. Taking responsibility for your commitments Protecting your family. Protecting your wealth. Having a plan for your wish list Ensure that you don’t have to live on hope and prayer or on alms due to any bad surprises in life. Designing your future the way you want it to be. And taking actions towards it and making course correction as we go along.

It is not about your money. It is about your life.

I was contemplating on why we celebrate Ganesh Chaturthi in such a weird way different from that any other festival. In general, the process of consecration of an Idol is extremely elaborate, has to follow numerous guidelines and can be conducted only by a few trained people. It also involves the use of resources of several kinds. But in Ganesh Chaturthi we bring in a Murti/Idol made of clay into our home every year, only to dump it in the sea or any other waterbody 10 days later.

On the surface this difference did not make much sense. But as in many things in sanatana dharma I realized how deeply thought through this festival was. While this festival addressed the economic concerns of potters whose trade temporarily ceases due to seasonal rains, Ganesh Chaturthi has a deep meaning for every family that celebrates it.

Creation of Ganesha and Wealth

Ganesha in the chaturthi festival is always made of clay. The clay that is otherwise freely available in the river banks and may collected by anyone without any licence or payment. With this clay, a beautiful murti/ idol is made. Ganesha is created from this through human efforts and dedication.

Wealth may similarly be created from freely available resources through efforts and dedication. There is a beautiful Jataka Tale of how a man became a big merchant starting from nothing but over heard advice and a dead mouse. While this has been true all along, it has never been more easier and common place than ever before. Billion Dollar companies that have started out from basement and a computer.

Manifestation of Wealth:

Ganesha is a very personal god. Almost all children are told to pray to pilliyar ummachi (an endearing way to address God used with children). In Chaturthi too Ganesha happily takes any form you want him to – from a military Ganesha, software engineer Ganesha, Ganesha playing classical hindustani to saxophone, nothing is quite out of bounds for him. Ganesha also happily uses instagram, whatsapp and is happy to adapt to current trends and technology.

Wealth too can take any form you want it. Gold ornaments, SUV, land, shares, PMS, Mutual funds, charities , business are all just various manifestations of your wealth. Wealth can take any form you want it to and can move from one form to another.

Celebration of Wealth:

Once Ganesha is installed Pooja is done every day, People are invited and Prasad is given. Every day is a celebration of the deity. People invite and visit each others house to take part in the celebration of the manifestation of God as well as take part in the blessings. They also contribute to the bigger mandals in the society, village, area etc.

It is not uncommon to see certain people believe wealth is accumulated only by depriving others. Unfortunately this thought was propagated a lot by movies of an era. However, Ganesh Chaturthi shows wealth too is a blessing that may be manifested through hard word, needs to be celebrated when possessed and shared among the community. When we can create God through our hands, what in the world can we not create.

Letting it all go:

Ganesh Visarjan

At the end of 3/5/7/11 days, Ganesha is immersed in a waterbody. Ganesha who came from the clay of the river banks, goes back to where he came from and he is sent off by each family with much fan fare and celebration. The families let go of their dear Ganesha who has become a part of their family, and brought in much grace and celebration, so that he can go back to where he came from.

As humans, we all back to where we came from. But even in the context of wealth, as in the four stages of life of a man – Brahmacharya, Grihasta, Vanaprasta and Sanyasi, man is to willingly give up the wealth earned through his work during his lifetime inorder to pursue higher realms of life. He does this willing and happily. He celebrates letting go of wealth, the way he celebrated manifesting and possessing it. He lets go not because he had to, as it leave it to his children after himself, but because it is time.

May this Chaturthi Ganesha bless us all with his immense knowledge to manifest, protect, grow and let go when it is time. Ganapati Bappa Morya, Managala Muti Morya.

Can money really solve your money problems? Can your sudden windfall of money be the worst thing that can happen to you in your life?

Does Money Really Solve your money problems? If not money, what else could solve it?

The Problem

Doesn’t that sound weird. How could a huge sum of money not solve all the financial problems I have today. I can hear many of you say, “Try me”.

I may not be in a position to conduct such a social experiment, but such things have already happened, many times before. Lottery Winners, Sudden inheritance, Prize show winners. Most of these people lose the money in under 5 years.

If you are still wondering, “How is that even possible. They must be really stupid, I’m not.”

An Example of the Right or the wrong Kind

Let us look at the life of Sushil Kumar.

In 2011, he was the first person to win 5 Crores in Kaun Banega Crorepati. Having come from a very humble background, it was more money than he had ever imagined. Certainly a person who won it in a quiz show like ‘Kaun Banega Crorepati’ has earned it. He must be no fool either. And it is the kind of money, that one could be set for life. We aspire to build a retirement corpus half that size to be able to retire and live a decent good life.

Did he live happily Ever After?

Sushil says his worst period of Life was after he won the game show. Out of Peer Pressure and to be able to say something to the people interviewing him, he invested in businesses he had no idea about. As a result was cheated by his business partners and lost most of the money. He got depressed and became an alcoholic which put immense pressure in his relationship with his wife. His wife was tired of him spending all day watching movies, drinking and wasting his life away. She left him to be with her parents and threatened divorce.

Sushil thought he could win his wife by becoming a Movie director. Like most people think they can run a restaurant because they love food, Sushil thought he could direct movies, because he loved to watch them. He moved to Mumbai hoping to make his dream of becoming a director come true. He spent most of his time smoking drinking and writing movie scripts. He even managed to sell one for 20,000.

Realization and Learnings

After falling into depression and a lot of introspection, he realized he was ‘not seeking to fulfill his dreams but is running away from the truth’. This was Susil’s learning from his rags to riches to rags story:

– Real happiness lies in doing the work of your choice – One can never calm certain emotions like arrogance – It is a thousand times better to be a good person than just being a ‘big celebrity’ – Happiness is hidden in small things – One must strive to help people as much as possible that that must start from his/her own home/village.

My Learnings

And what is my learnings from this story.

If you had not learned how to manage and live well with the money you have, no amount of money can solve your money problems.

If you don’t know what you want to do other than work, you are not ready to retire.

What are your learnings and what actions are you going to take? Leave it in the comments.

How two Batsmen with completely different styles brought victory to the Indian team and what investing lessons can we learn from the two

India’s most followed religion – cricket has a lot Investing lessons for us. Let’s look at two successful Batsmen of recent times and see what they teach us about Investing.

Pant, the Aggressive Investor

Pant is a big hitter. He is most known for his fastest 50’s and 100’s. He has won some big matches for the country. The aggressive style of playing has at times cost the wicket too early in the match not giving a chance to make any impact in the score board.

An Aggressive Investor is someone who is betting on a few multi baggers to get good portfolio returns. They are not shy of the hero or zero trades, where they may lose in most trades, but a few good ones will likely compensate for the lost ones.

Pujara, the Conservative Investor

Chetaswar Pujara said this in a recent interview with ESPN.

“If I am successful with my method, I don’t need to take any risk. Even if you hit over the top, you just get four runs, and two extra if you clear the fence. So the question is whether it’s worth the risk.”

Here is a man who understand his style and understands risk. There is a great parallel to this in the investment.

Pujara is the kind of Investor who puts most of his money to government guaranteed schemes such as PPF, NSC, KVP etc. He is ok with returns on par or may be even below inflation as long as it consistent and has sovereign guarantee.

Are you Pant or Pujara ?

In Investment the most important question is to ‘Know thyself’. How much time are you willing to put to learn something, how much risk can you take which means how much money are you willing to lose, what is your investment tenure, How disciplined are you?

Playing in the net practice is not the same as playing in a real match ! A back tested strategy with high win % may not work for you as it does not suit your style.

Before you go looking for answers, look for the right questions to ask and know yourself.

is a lovely popular quote that is most certainly wrong says Dan Gilbert, Harvard Psychologist and author of ‘Stumbling on Happiness’.

Money provides an “opportunity for happiness,” the authors say, since moneyed people can live longer and healthier lives, enjoy financial security, have leisure time, and control what they do every day.

Dan Gilbert in the paper titled,

‘If money doesn’t make you happy then you probably aren’t spending it right.’ – talks about the right way to spend money to optimize happiness. So how do we do it?

(1) Buy Experiences instead of things

The best memories I have of my childhood were those I was on vacation with my family. The best memories of my adult life were also in obscure mountains and long road trips. However, I don’t think our trip around the could have been any better if we had travelled in a sedan over a hatchback. We like experiences more because we anticipate and remember them, the research says, and we appreciate them longer.

(2) Spend money to help others instead of yourself.

The money we willingly spend on others gives us a greater joy over those that we spend on ourselves. Look around you and see who you can help out. The pandemic has given us all a opportunity to do that to those unfortunate around us.

(3) Buy many small pleasures instead of few big ones.

Random gifting of a single rose and love notes multiple times during the year would bring net more happiness to your spouse than an elaborate exquisite dinner in Taj and a DeBeers Diamond Necklace during anniversary.

(4) Buy less insurance for “GOODS”

Extended warranties, replacement guarantee for the LED display, generous return policies may actually under mine happiness as we get used to good and bad things equally fast.

(5) Pay now, consume later

We are in the culture of use now, pay later, but it is the delayed gratification of desires that gives the most amount of happiness for most of the happiness is in the anticipation more than it is possession itself. Planning a vacation was fun, saving for it monthly gives you the anticipation that prolongs it, rather than putting it on your credit card and having to pay for it later.

(6) Think about what it’s really like to own the thing you want to buy

The cabin in the woods would have mosquitoes, your swimming pool will need to be cleaned, your beach house will be dirty with sand the furniture will get spoiled faster with salty air. Owning things in actuality are not as good as they show in ads. So give it a long hard thought !!

(7) Stop the comparison shopping

What is otherwise known as keeping up with the Jones. Too many people end up with bigger than necessary houses, Tv’s, Car’s because they are trying to impress somebody like parents, spouse, Ex’s, colleagues etc. If you let your buying decisions be determined by the matching or bettering what someone else has- that my friend is a bottom less pit.

(8) Ask your friends.

Your friends know you better than you know yourself. Your friends can tell with better accuracy who you should date, which of your relationship is likely to work out for you. You are too invested and bit to blind to see those things for yourself. So next time do ‘ask a friend’

It’s not the toys that makes the child happy but the play. It’s the same with you too. Rather than adding bigger, faster and fancier gadgets (toys), spend your money well and buy happiness.

Based on : “If money doesn’t make you happy then you probably aren’t spending it right.” by Dan Gilbert

How the power of compounding enabled one temple to accumulate trillion of dollars in its treasury and how you can use the same technique too.

A few years ago, some of the vaults of Padmanabha Swamy Temple in Thiruvandhapuram was opened as per the order of the Supreme court. The vaults had tons and tons of Gold Coins, Crowns embedded with precious stones, Gold Jewels with embedded diamonds, Statues of Gold , Diamonds and various other precious stones were found. There were many discussions on who should be allowed to manage the temple and its treasure.

But to me the important question was “how did this one temple amass such huge fortunes?”

I found my answer when I visited the temple and the museum in the Kudramalika Palace nearby. Travancore Kings considered their kingdom as God’s own country and themselves as only representatives appointed to administer the province. The Deeply religious kings visited the Padmanabhaswamy temple every year on his birthday and contributed to the temple treasury Gold equivalent to their weight.

This practice called Thulabaram is very popular all throughout Kerala even today. Although people give different things like coconuts pulses etc and not Gold unlike the Kings.

It is this practice that had been followed across generation of Travancore Royal Family that was one of the chief reasons of this huge treasure estimated to be a trillion dollars worth. This was also the reason probably supreme court has vested the rights of temple administration back to the unbroken dynasty of the Travancore Royal Family.

The compounding can work as well for you as it had worked for Lord Padmanabha. If you cannot contribute Gold equivalent to your weight every year, may be you can still start an SIP every month. May be you don’t have the few hundred years that Lord Padmanabha and the Travancore Raja Samsthanam had, but neither are you trying to build a vault with tons and tons of Gold. All that we hope to have is a peaceful retirement life without having to worry about keeping up with ever rising inflation and a few decades of your life should be sufficient to do the same.

So how are going to make time and money work for you?